Valuation: One of The Best Indicators of Performance

Mar 14, 2025Since 2022, investors have largely been rewarded for snapping up the fastest growing companies, regardless of valuations. But with a potential cloud hovering over the U.S. economy, and the changing winds of a new administration in full swing, before buying, we believe it is finally time ask: “but at what price?”

Today’s economic environment is characterized by a seemingly hazy climate. While U.S. investors grapple with headlines of tariffs and a possible recession akin to the old one-two punch every week, markets outside the U.S. appear positioned for triumph. In the face of uncertainty, U.S. investors have been reminded that earnings growth cannot remain perpetually above historical averages forever, and index returns are unlikely to be driven by further multiple expansion. We have discussed this multiple expansion conundrum in past thought pieces. With that said, we believe valuations are shaping up to be one of the most important investment factors in the coming years, and investors need to be cognizant of how much they are paying for a company’s earnings.

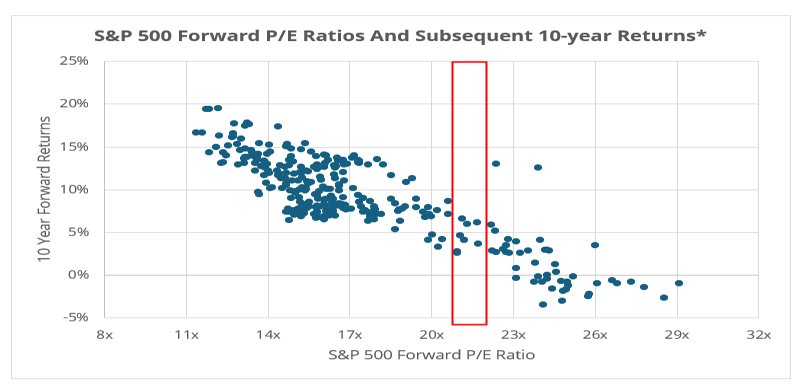

*Annualized returns including dividends. Data from 6/29/1990 – 2/28/2025 Source: Bloomberg L.P.

*Annualized returns including dividends. Data from 6/29/1990 – 2/28/2025 Source: Bloomberg L.P.

The chart above represents the relationship between the S&P 500 forward Price-to-Earnings (P/E) ratio, and the subsequent 10-year total returns, with the red box indicative of the current correlation. Even with the recent pullback in U.S. markets, the index still looks quite expensive relative to history. The previous two years were anything but average, with 20%+ returns; however, we have entered a new, apprehensive environment. Elevated valuations need the support of continued earnings growth, which will be challenged by interest rates remaining higher for longer, sticky inflation, and global tariffs. Considering these obstacles, we believe buying stocks at today’s multiples is not indicative of the high returns we have seen in recent years.

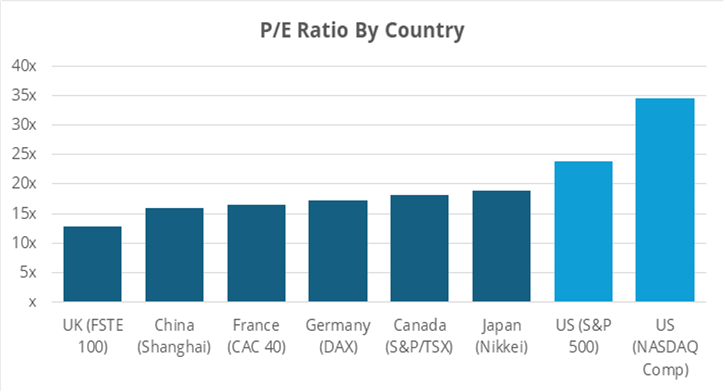

*Data as of 3/12/2025. Source: Bloomberg L.P.

To be clear, this does not mean that the world is currently un-investable. Although the domestic market is still priced near perfection, as the graph above illustrates, the rest of the world is pricing in some of the worst-case economic scenarios. As an active global value manager, our job is to seek the best opportunities, both at home and abroad. We believe that U.S. trade policies are catalysts to push foreign nations to spend more on infrastructure and defense, an expansionary fiscal tool. We have observed this in Europe’s recent push to increase their defense spending, with positive remarks from Germany, France, Italy, and the U.K.

Our global portfolios are currently overweight Europe. However, we continue to look for new direct and indirect opportunities to capitalize on what we believe are the early innings of this multi-year trend towards fiscal expansion that we intend to capitalize as we seek to deliver the best possible risk-adjusted returns possible.

We encourage you to contact your MAP representative with any questions or concerns.

Managed Asset Portfolios Investment Team

Michael Dzialo, Karen Culver, Peter Swan, Zachary Fellows, John Dalton, and Nicolas Vilotti

March 14, 2025

Certain statements may be forward-looking statements and projections which describe our strategies, goals, outlook, expectations, or projections. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied by such forward-looking statements. The information contained herein represents our views as of the aforementioned date and does not represent a recommendation by us to buy or sell this security or any other financial instrument associated with it. Managed Asset Portfolios, our clients and our employees may buy, sell, or hold any or all of the securities mentioned. We are not obligated to provide an update if any of the figures or views presented change. Past performance is no guarantee of future results.