About That Inflation...

Jun 04, 2021In May of 2020, we wrote about the potential for an uptick in inflation. As the world continued to grapple with the coronavirus, the United States attempted to thread the economic needle. Record-breaking fiscal stimulus was passed in record time. Thankfully, the U.S. has been able to avoid the most negative potential economic outcomes.

However, the seemingly unlimited fiscal and monetary stimulus seen in the past 14 months will have consequences. We believe part of these consequences will show up in the form of inflation. We already see the crystallization of inflation: houses are being bid up to well-above their pre-pandemic values, labor shortages are building, and raw material prices are surging.

This will affect the economy, markets, and your portfolio. The U.S. has lived with minimal inflation for 30 years and has not seen the Consumer Price Index (CPI) top 5% since the early 1990s. You have to look back to the early ’80s to see CPI rising above 10%. While we think inflation nearing 10% is unlikely, we believe a base case of a CPI rising 3-4% is reasonable given the current circumstances.

Most investors in today’s market have little to no memory of markets in times of inflation. However, positioning your portfolio to at least dull the effects of inflation is a necessity.

The Forces of Inflation

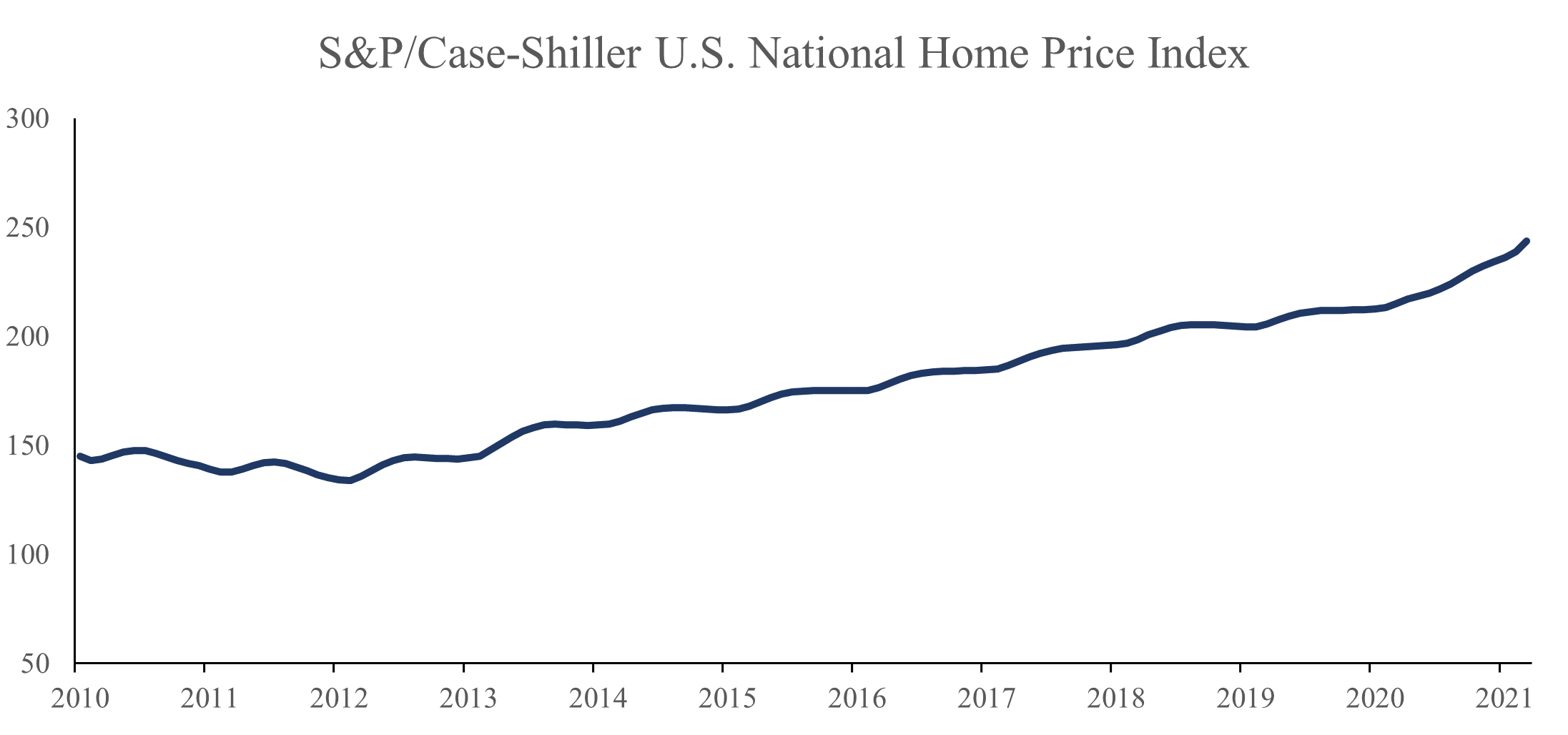

We are already hearing alarms ringing. Used car prices are up between 15%-25%[1], the Dow Jones Commodity Index is up 40% from pre-pandemic levels, and prospective home buyers are seeing rapidly rising prices.

Last May, we talked about factors leading to inflation: demand-pull and cost-push. We see both issues on the horizon or already here.

The Demand-Pull

Over $5.5 trillion in fiscal stimulus and relief has been signed in the U.S. since March 2020.[2] That is nearly 1.5 times the annual tax revenue collected by the United States government. This money has been essential to avoiding economic catastrophe. The low income and low middle-income consumers absorbed the brunt of the economic blow; however, government stimulus and unemployment aid were able to make up for the bulk of lost wages. Meanwhile, upper-middle and upper-income consumers able to work from home were largely (but not totally) unscathed by the economic impact of COVID.

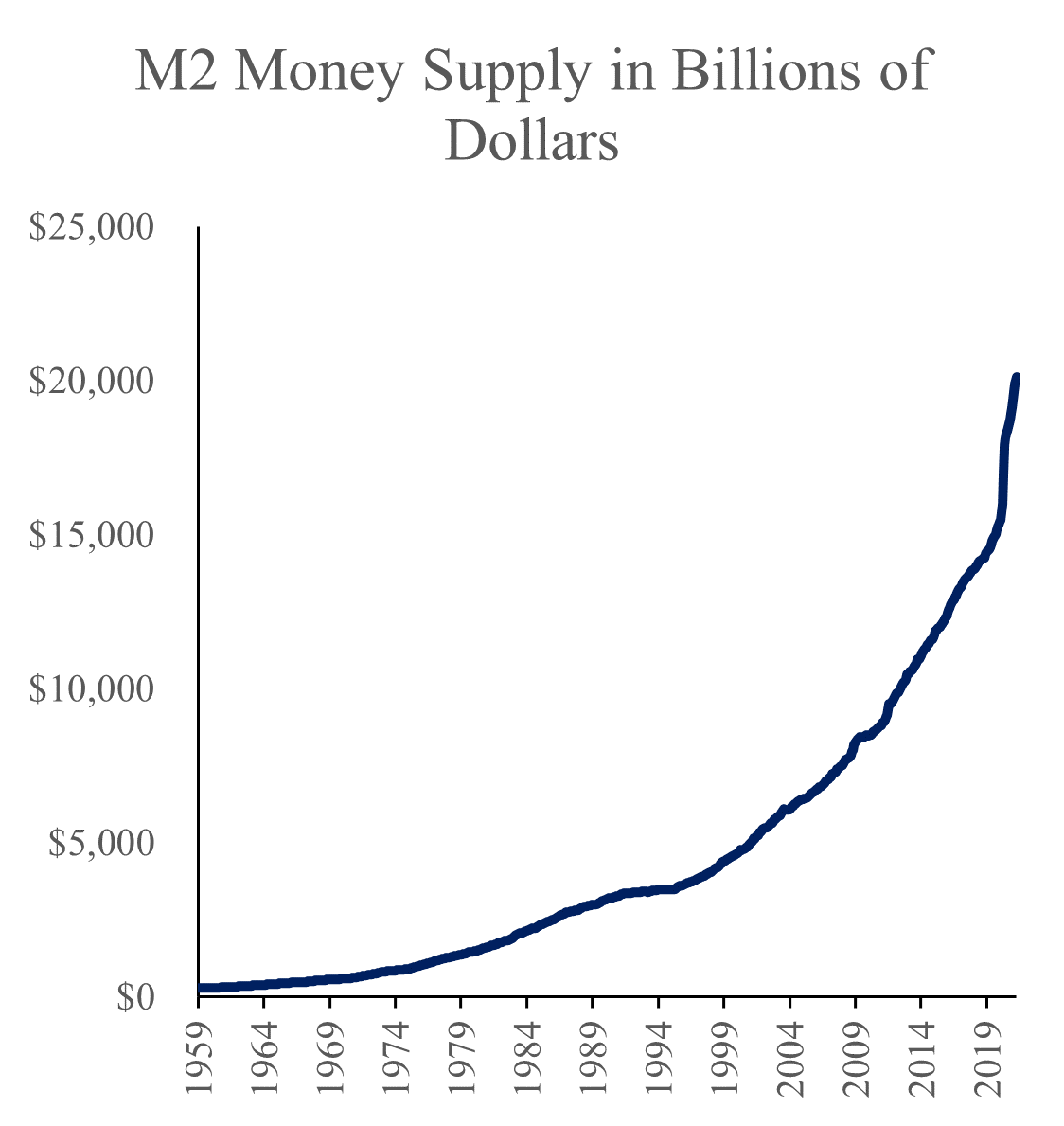

In fact, America has seen a savings boom due to the government supplementing lost wages and muted discretionary spending from higher-income consumers. Both the savings rate and the M2 money supply (currency held by the non-bank public, checkable deposits, travelers’ checks, savings deposits, small time deposits under $100,000, and shares in money market retail funds) have skyrocketed since the beginning of the pandemic:

As fear of the virus continues to drop and more people have the desire and means to spend, prices should rise, especially for discretionary goods. Pent-up demand for travel is real. Pent-up demand for housing is real. In the long term, calls for increased infrastructure spending and the developed world’s green agenda will require massive amounts of government spending.

This increase in spending will require increased supply to avoid inflation. However, we continue to see problems throughout global supply chains, which leads us to the next issue: the cost-push.

The Cost-Push

At the beginning of the pandemic, companies were laying off employees, delaying large capital expenditures, and reducing inventories. Cost-cutting was implemented due to lower demand and a projection of the worst-case scenario. As demand has begun to pick up, supply chains have had trouble keeping pace.

Shortages are already beginning to percolate. Restaurants are having difficulty filling open positions and even obtaining condiments. Large-scale commodity projects were largely delayed as market uncertainty discouraged producers from large expenditures. Now, commodity prices are rising as the world returns to normal, and supply is slow to return. As the cost of inputs rise, the price of finished goods will face upward pressure.

Computer chips, a key input for every technology from calculators to tablets to vehicles, face critical shortages. Intel believes these shortages could last several years as capacity is slowly expanded.[3] Meanwhile, producers are feeling the heat from the chip shortage. For example, auto manufacturers have had to idle plants and delay the release of new vehicles due to the lack of available chips; simultaneously, demand for vehicles is soaring.

Additionally, the United States’ most prolific trade partner is openly mentioned as an adversary by both sides of the aisle. Indeed, one of the very few things both sides of the aisle can agree on is that China is becoming a threat to America’s world order. “Taking on” China will require shifting supply chains elsewhere. These shifts come with a cost.

Labor, raw material, and chip shortages and changes will continue to increase costs throughout the supply chain, a cost that the consumer will increasingly bear.

Fuel on the Fire

Since the beginning of the pandemic, the U.S. government has responded by easing monetary policy and distributing fiscal stimulus. The current administration has proposed a $1.7 trillion infrastructure bill and a$1.8 trillion bill to address child-care, access to free education, and paid family leave. The more progressive wing of the Democratic party wants even more stimulus.

Government stimulus creates more demand in the system when funded by debt, as it creates more money purchasing more goods. As we stated in the previous section, it will be difficult for supply chains to keep up as consumer demand returns to the system – adding sustained high levels of government spending could be fuel on the fire.

When it comes to government debt and fiscal spending, it will be difficult for either party to slow down. Republican efforts in the Georgia special elections were certainly not helped by party legislative leadership’s refusal to approve $2,000 stimulus checks. While the GOP is currently negotiating the sticker price of the Biden administration’s most ambitious proposals down, we believe it will be politically untenable for either party to cut spending drastically.

Voters have simply come to expect more help from the government. It is very painful to stop inflation with high-interest rates that often force a recession, so either party in power will be reticent to slow down the economy and lower fiscals pending. Further discouraging interest rate hikes is the large and ballooning public debt load. Interest expense as a percentage of GDP would rise dramatically if rates increase much off of their current low levels. This creates a recipe for sustained inflation.

Potential tax hikes could soften the inflationary pressure from increased government spending. More money would be taken out of the hands of the private sector and placed in the hands of the government, which would be inflation-neutral or even deflationary. However, the tax hikes making the rounds in the Biden administration would be unlikely to cover sustained high levels of government spending.

Preparing Your Portfolio

So, how should one position themselves to protect against inflation? Broadly speaking, the industries that should perform best during periods of inflation either:

1. Sell goods or services that are necessities and can thus pass their increased costs onto consumers. Think utilities and healthcare.

2. Companies which have strong brands that can increase prices.

3. Sell products that, by the very nature of inflation, will see price increases. Think commodity sellers like companies in the materials and energy industries.

MAP has positioned its clients’ portfolios to take advantage of the above categories. We have exposure in healthcare, utilities, and materials, and part of our process is to identify companies that we believe have strong brands.

Additionally, we continue to espouse the benefits of global investing. Because we invest outside the U.S., our portfolios have a natural hedge against inflation. Each country we are invested in will face varying inflation levels, so avoiding single-country risk means avoiding single-country inflation risk.

Finally, we believe value is set up to outperform growth during times of inflation. Rising inflation has historically caused interest rates to rise. As interest rates rise, the values of all companies are affected negatively, but the values of growth stocks are hurt disproportionately more due to the time value of money. Value stocks are valued more considerably from near-term cash flows, while growth stocks are valued based on cash flows in the distant future. When interest rates go up, the value of those distant cash flows decreases more than the value of near-term cash flows.

Value stocks started to outperform growth stocks earlier this year, partially due to the market beginning to account for the potential for higher inflation. Growth stocks have benefited from low-interest rates for many years, and there may finally be a reversal of fortune.

Managed Asset Portfolios will continue to take a diversified approach. We believe inflation is here to stay in the near term, but the team will continue to identify investment candidates based on individual merits. This has been the key to our success and one of the essential ingredients to how we think about investing.

Managed Asset Portfolios Investment Team

Michael Dzialo, Karen Culver, Peter Swan, John Dalton, and Zachary Fellows

June 2021

The information contained herein does not represent a recommendation by us to buy or sell any security or securities mentioned within this presentation. Certain statements may be forward-looking statements and projections which describe our strategies, goals, outlook, expectations, or projections. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied by such forward-looking statements. Past performance is no guarantee of future results.

[1] https://www.forbes.com/sites/edgarsten/2021/06/01/used-vehicle-pricing-hits-bizarre-levels/?sh=2a3450329833

[2] https://www.investopedia.com/government-stimulus-efforts-to-fight-the-covid-19-crisis-4799723

[3] https://www.reuters.com/technology/intel-reiterates-chip-supply-shortages-could-last-several-years-2021-05-31/